Global chargeback volume is projected to reach 337 million transactions by 2028, costing merchants over $40 billion annually. Behind every one of those numbers is an analyst on a queue. According to ACAMS, 67% of fraud and AML analysts report moderate to severe burnout, with alert volume cited as the leading cause. Average fraud analyst tenure is now 2.1 years, compared to 3.8 years for other risk roles in financial institutions.

The problem is not detection. Detection is working. The problem is what happens after detection. Fraud teams operate with false positive rates of 90 to 95%, which means analysts spend the majority of their working hours investigating transactions that turn out to be legitimate. They clear 80 plus alerts per shift, and genuine fraud accounts for less than 2% of total volume.

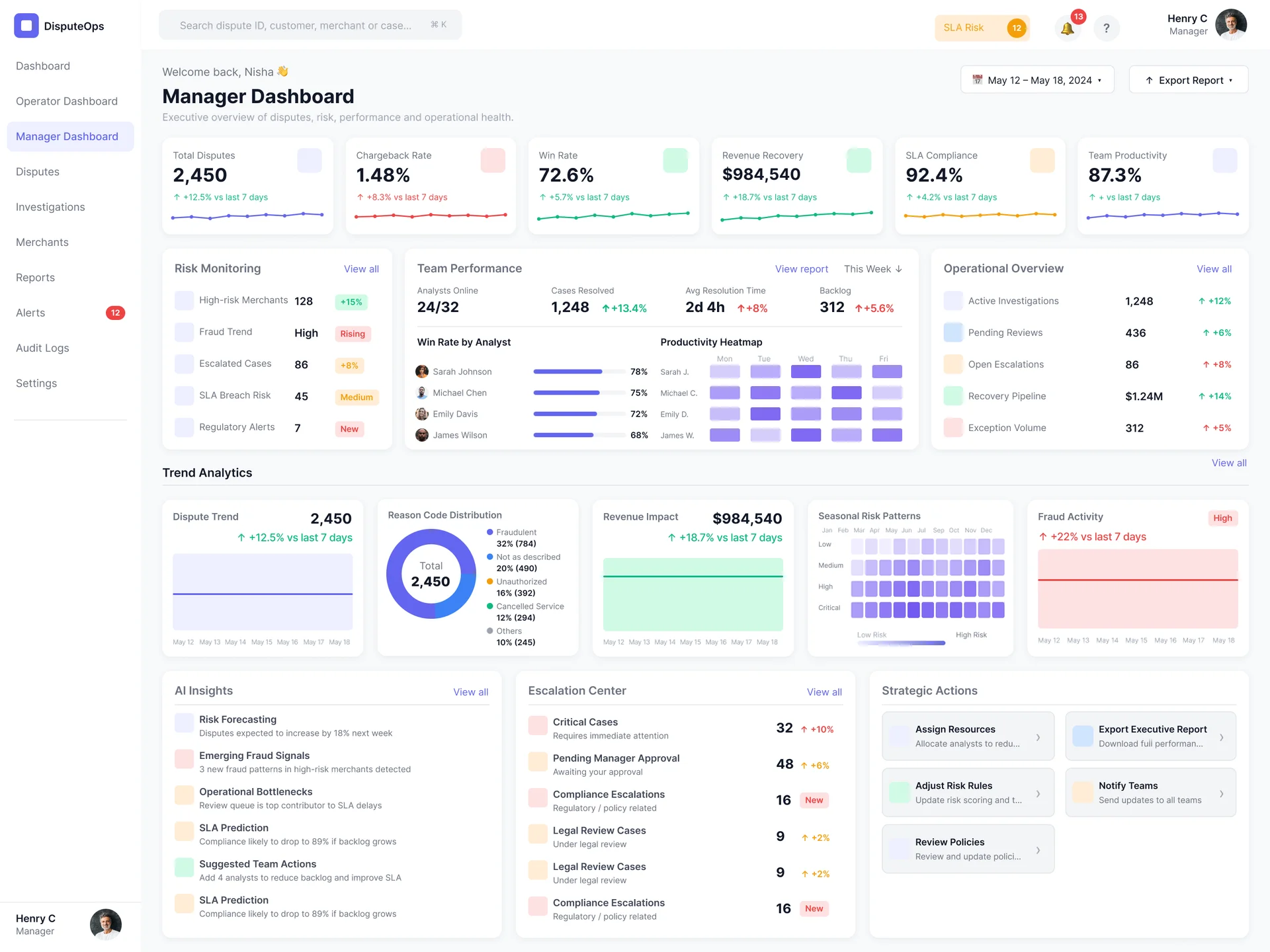

The dashboards meant to help them have not kept pace. Analysts move between five to ten separate tools to investigate a single case. Asana's Anatomy of Work Index found knowledge workers switch between apps 25 times per day. UC Irvine research established that it takes 23 minutes and 15 seconds to fully regain focus after a significant interruption. Payment operations is the sector where this cost is the most expensive, and the least talked about.